Pass The Vermont Life, Health, Property & Casualty Insurance Test

Vermont Life, Health, Property & Casualty Insurance Practice Exams

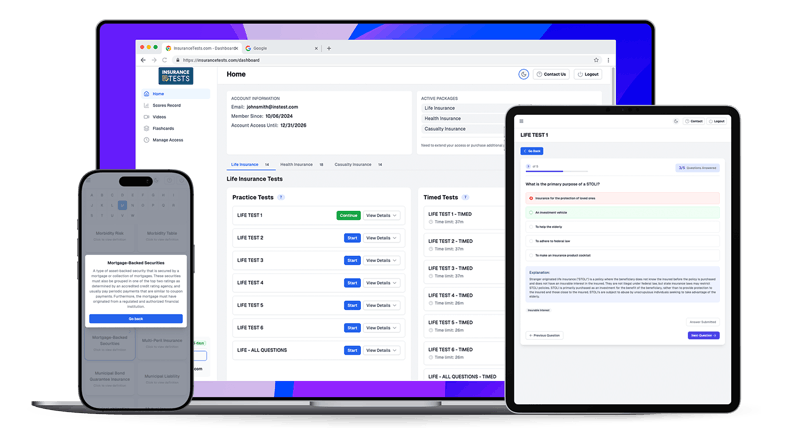

Pass the Vermont Life, Health, Property & Casualty Insurance test with confidence! Don't rely on the outdated material on other Vermont Life, Health, Property & Casualty Insurance practice test sites. Our program comes with 1,000 Vermont Life, Health, Property & Casualty Insurance exam questions with detailed answer explanations similar to the ones you will find on the actual Vermont Life, Health, Property & Casualty Insurance exam. All of our Life, Health, Property & Casualty Insurance tests are up to date with latest 2025 material for Vermont.

Our online Vermont Life, Health, Property & Casualty Insurance test prep has helped thousands of test-takers pass their insurance exam and comes with a 100% Pass Money-Back Guarantee!

Vermont - Life, Health, Property & Casualty Insurance Free Trial

Pass The Insurance License Test

Our Insurance practice exam prep has national questions with detailed answer explanations. That’s 300 insurance practice exam questions for each insurance area, 500 questions for a paired combo and 1,000 questions for all four areas, plus every paid user gets vocabulary study flashcards with insurance terms and definitions. Our insurance practice exams are also up to date with the latest insurance regulations. Since our practice insurance tests focus on some of the most popular national insurance material, our questions apply in every state and U.S. jurisdiction.

Our insurance exam prep comes with a 100% Pass Money-Back Guarantee, and has helped countless others pass their insurance test!